Art: Investing vs Collecting

Art: Investing vs Collecting

Society's favorite store of value, fine art fails as a compelling investment. Although nascent, digital art on blockchain makes a better alternative asset and complement to an investment portfolio.

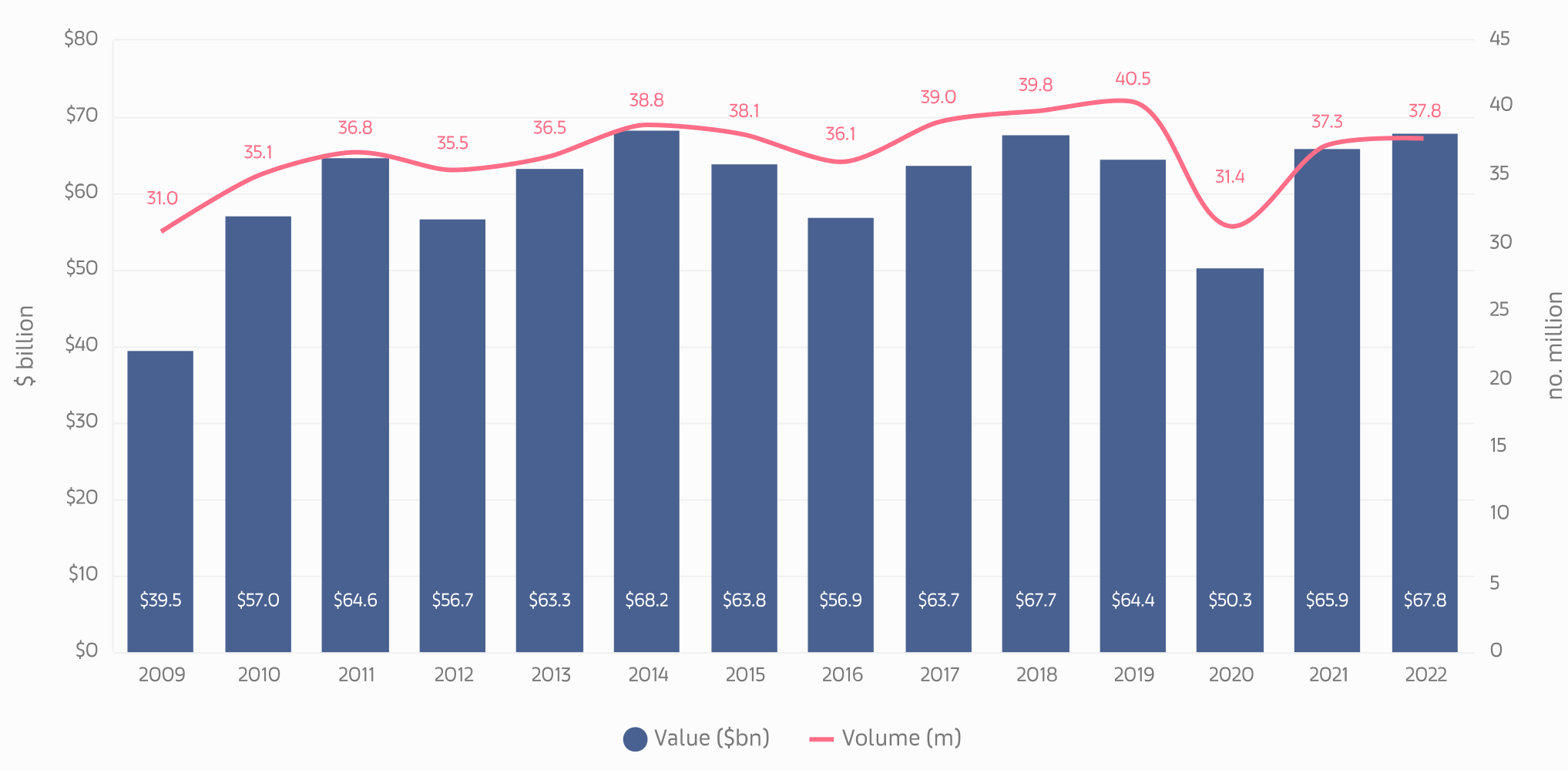

All-time high sales, but profits remain challenging: Driven by expanding wealth and the scarcity of premium artworks, art sales have been on the rise, reaching a remarkable $68 billion in 2022, second only to the peak of $69 billion in 2014. Despite the attention and impressive figures, investing profitably in art presents a significant challenge. While art has historically served as a stable asset with unique risk-reward characteristics, the complexity of the modern art market makes turning a profit more elusive than it appears.

The attractive illusion of art indices: Art indices, such as the Sotheby's Mei Moses Index and Artprice, often serve as the main reference for prospective investors. These indices estimate annual art market returns at 9%-15%, providing a strong case for including art in investment portfolios. However, they have inherent limitations. These indices primarily represent higher-value artworks, accounting for only a tiny portion of the art market. They rely on public auctions, overlooking private transactions that make up a significant portion of market turnover. Furthermore, unlike financial asset indices like the S&P 500, art indices are not investable, and replicating index returns is not feasible. As a result, they fail to accurately capture the investment experience of most art buyers. The complexities of transaction prices, positive skewness in returns, long holding periods, and concentration of art collections exacerbate the issue, creating a skewed impression of average returns in the art market.

Flashy headlines distort reality of art investing: While attention-grabbing nine-figure sales of individual artworks make headlines, they offer a distorted perspective of investment returns in the broader art market. A closer analysis of record-breaking auctions, such as the late Paul Allen's $1.6 billion auction, reveals underperformance compared to the stock market, with a 6% return versus the S&P 500's CAGR of 9% over the past 18 years. Similar results emerge when examining John Maynard Keynes' $100 million art collection. Despite being visionary collectors with substantial resources, their art investments performed worse than a typical 401(k) account. While the allure of art as an investment is undeniable, the true 'return on investment' for many may lie more in the joy of collecting and appreciating art than in its financial yield.

Digital art on the blockchain: a different asset class? As a nascent asset class, digital art on the blockchain holds potential differences from traditional art. It boasts efficiency and transparency, with lower barriers to entry for collectors. The collector base is more fragmented and diverse, including long-term holders contributing to market stability and speculators creating liquidity. With $1 million, one can create an investment portfolio representative of the current digital art market (collectibles: 72%; generative art: 15%; other art: 13%). While digital art has yet to prove itself as a store of value like traditional art, it offers the most compelling risk-reward among alternative asset classes, without the need for meticulous selection of individual investments.

Art is the oldest asset class in history

Art collecting goes back thousands of years and can be traced to various ancient civilizations.

Pharaohs in ancient Egypt amassed significant collections of art and artifacts. Many of these items were created for the purpose of accompanying them into the afterlife. The discovery of the tomb of Tutankhamun in the early 20th century revealed an extensive collection of such objects, including jewelry, statues, and the famous gold funerary mask.

Wealthy Romans were known for their extensive collections of art and other cultural artifacts. Many of these collections included Greek statues, paintings, and vases. Art was often used to adorn their homes and public spaces, showcasing wealth, power, and taste. A well-known example is the Villa of the Papyri in Herculaneum (a city destroyed, like Pompeii, by the eruption of Mount Vesuvius), which had an extensive collection of bronze and marble statues and a library of around 1,800 papyrus scrolls.

Collecting art and cultural artifacts has deep historical roots, reflecting a longstanding human desire to surround ourselves with objects of beauty and cultural significance. The Medici family in Florence (15th-18th centuries) is one of the most well-known patrons of arts who amassed an immense collection of art and rare books. They commissioned works from artists like Michelangelo and Botticelli, demonstrating their passion for the beauty and intellectual stimulation of the arts, while also highlighting their wealth and influence.

King Charles I of England (1600-1649) was an avid art collector who amassed one of the most extraordinary art collections of his age, including works by artists such as Titian, Raphael, and Holbein. For Charles, collecting art was not only about personal enjoyment and aesthetic appreciation, but also about projecting an image of wealth, taste, and power.

Isabella Stewart Gardner (1840-1924) was an American art collector, philanthropist, and patron of the arts. She amassed a significant collection of European, Asian, and Islamic art. Her collection, housed in the Isabella Stewart Gardner Museum in Boston, includes works by Titian, Rembrandt, and Vermeer. Gardner was driven by a deep appreciation for art and the desire to create a cultural institution for the American public.

The 5 P’s of art collecting

Art collecting has been a passion for many throughout history, and it continues to captivate new generations of enthusiasts. The motivations for collecting art vary greatly.

Passion: Many people collect art simply because they love it. They find joy, inspiration, and personal fulfillment in the beauty and creativity that art provides. For these collectors, each piece in their collection often carries a personal significance and represents a unique aesthetic experience.

Preservation: Art is a reflection of society and culture. Collecting art can provide a deep sense of connection to a particular culture, period in history, or movement. It also allows collectors to preserve and share these cultural artifacts with future generations.

Prestige: For some, art collecting is a status symbol. Owning rare or important works of art can signify wealth, refinement, and sophistication. The social prestige associated with art collecting can be particularly attractive to some collectors.

Profit: Art can be a potentially lucrative investment. Some collectors buy art with the hope that it will increase in value over time. While this is not a guarantee, and art markets can be unpredictable, there have been many instances of artworks significantly appreciating in value.

Philanthropy: Some collectors view their art collections as a part of their legacy. They may plan to donate their collection to a museum or other institution, or pass it down to future generations. In this way, art collecting can be a form of philanthropy and a way to contribute to the cultural enrichment of society.

These motivations are not mutually exclusive. A single collector might be motivated by a love of beauty, the thrill of the hunt for a new piece, the desire for social prestige, the potential for financial gain, and the wish to leave a lasting cultural legacy. Each collector's motivations are as unique as the artworks they collect.

Art as an investment

While the rich tapestry of art collecting is woven from a multitude of motivations and personal passions, there is one strand that stands out for its practical and potentially lucrative nature – art as an investment.

This concept is not new; the wealthy patrons of yesteryears, from the Pharaohs of Egypt to the Medici family and King Charles I, were not only accumulating art for its aesthetic appeal or social prestige, but they were also, consciously or not, investing in assets that held their value over time.

The artworks they collected have not only survived through centuries but have grown exponentially in value. The gold funerary mask of Tutankhamun, for instance, is priceless today, and the artworks commissioned by the Medicis, some of which now adorn the walls of the Uffizi Gallery in Florence, are considered invaluable treasures.

Art as an investment becomes even more relevant in our modern economy. Over the last few decades, traditional assets like stocks, bonds, and real estate have been subject to dramatic fluctuations, leading investors to explore alternative investment opportunities. Art has emerged as an appealing option due to its potential for significant returns and its generally low correlation with traditional markets.

This was especially obvious in times of economic uncertainty such as the oil crisis in 1990, the dot-com bubble in 2000, the financial crisis in 2007-09, and the most recent COVID-19 pandemic. Investors actively sought out "safe-haven" assets that could retain their value. As one of the oldest assets, art, especially works by blue-chip artists, became widely regarded as the safe haven.

In the last 50 years, collecting art has become a strategic move, a method of wealth preservation and growth, and an opportunity to diversify investment portfolios. Hundreds of wealthy individuals have successfully amassed substantial wealth through strategic art collections. The late businessman and philanthropist Eli Broad and his wife Edythe owned an estimated $2.2 billion worth of art, including works by Jeff Koons and Cindy Sherman, which formed the core collection of the Broad, the art museum they built in Los Angeles. Likewise, the founder of the luxury group Kering François Pinault has been collecting contemporary art for over four decades. His collection, worth an estimated $1.2 billion, features over 3,000 works by artists like Damien Hirst and Jeff Koons.

Art collecting is on the rise

Art sales volumes reached $68 billion in 2022, second only to the 2014 result ($69 billion). Ultra-high-net-worth individuals with net worth of $30 million or more represented over 90% of art purchases. Around the world, there are nearly 200,000 of such ultra-high-net-worth individuals. These individuals on average allocate about 4% of their portfolio to art and other luxury collectibles.

Global art market sales: 2009-2022

At $1.7 trillion, art is a massive asset class, comparable in size to private debt ($0.8 trillion) and private equity ($3.4 trillion). The total value of art expanded nearly 10X in the last 50 years. Appreciation has been driven by three key global factors:

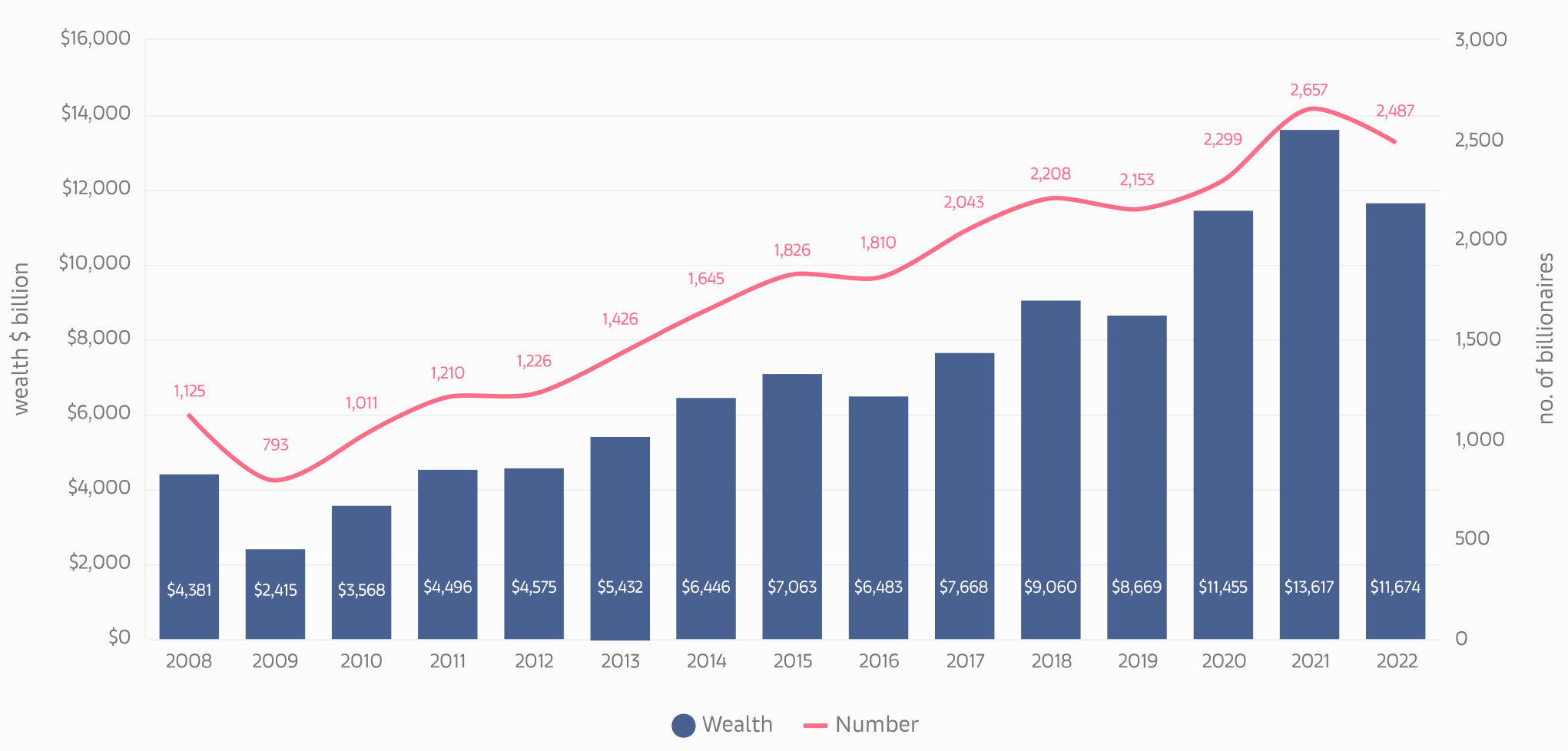

growth in the purchasing power of the ultra-high-net-worth community (billionaire wealth has more than doubled in 10 years and reached $11.7 trillion in 2022)

diminishing supply of available artwork (as it is acquired by museums and permanent collections), and

international marketability of the asset.

Global Billionaire Population and Wealth 2008-2022

As the number of millionaires and billionaires continues to increase, so will the art sales and values. Surveys of HNW collectors by Arts Economics conducted in collaboration with UBS, showed that collectors were spending more in 2022 than they had prior to the pandemic, including a greater share at the high end of the art market. The proportion in the $1 million-plus range increased from 18% to 31%, and at the $10 million-plus level had doubled (to 12%). Seventy-seven percent of HNW collectors remained optimistic about the global art market in 2023. The surveys also indicated strong spending plans for this year, with a majority (55%) planning to buy art in 2023, including 65% in the US.

The shift of sales online is a major tailwind which is expected to drive art sales for many years to come. The share of online sales increased to 16% in 2022 from 9% in 2019. By making art more accessible online, there certainly has been more evidence of progress in the trend towards democratization. Online access to dealers, auction sales, and fairs has allowed much wider access to new audiences, with 40% of dealers’ online sales being to brand new buyers. Online bidding and buying have been identified as the key channel for gaining new buyers in the auction sector, as well as providing a means for existing collectors to access the market in more sustainable ways, without the pressure of attending every event in person.

Is art worth investing?

Art is an unusual asset for many reasons, including the owner’s emotional attachment to it. Nevertheless, if you are acquiring art for significant prices, it is an asset.

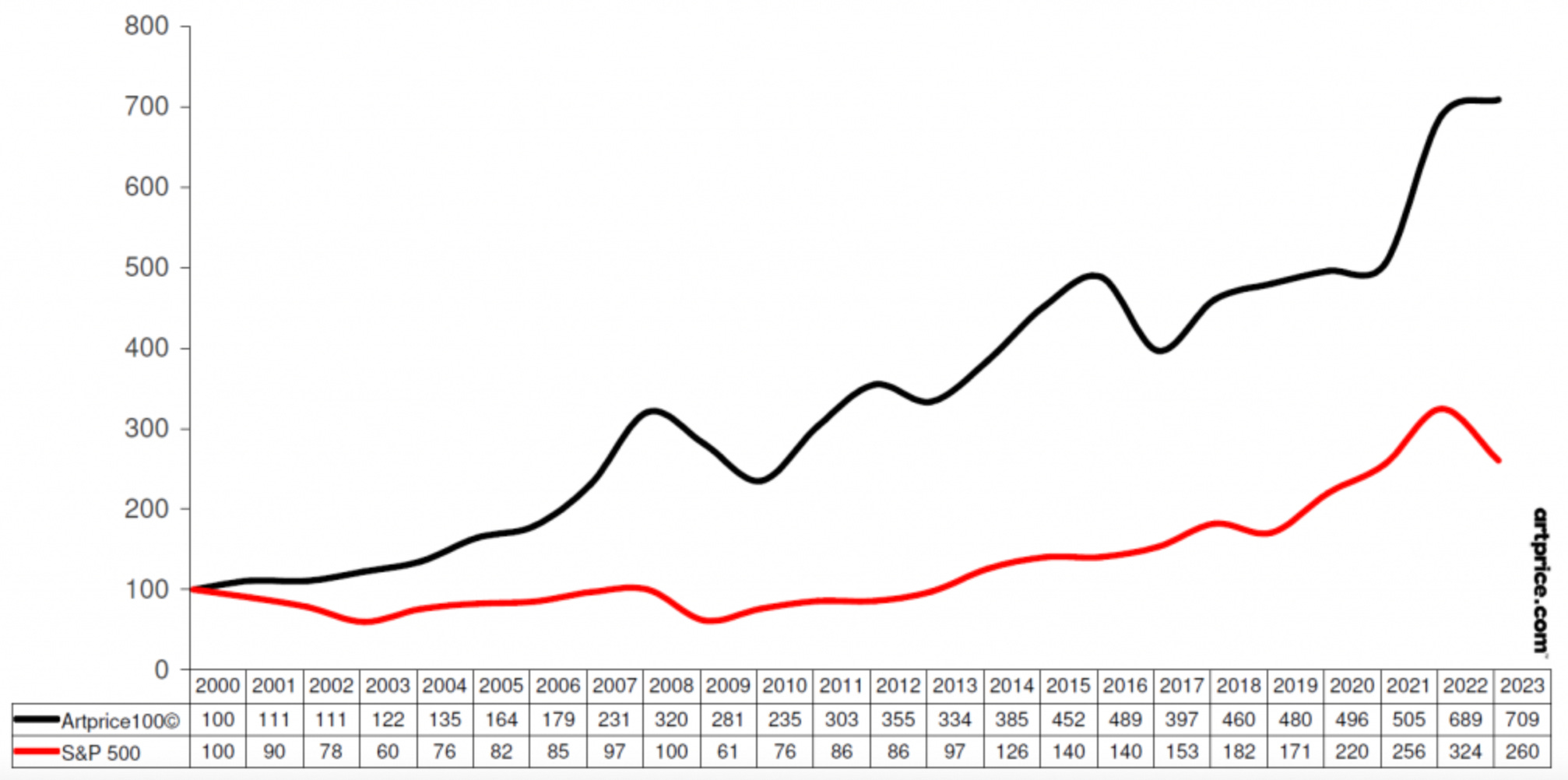

Collecting art is widely regarded as a lucrative endeavor. According to a report by Artprice, the global art market posted annual returns of 9% from 2000 to 2023. As a sales-based indicator, the Artprice index reflects a purely financial approach to art and reveals the hypothetical financial result one would obtain if they were to invest in the world’s top-selling artists to benefit financially from their success.

Masterworks, the company enabling fractional ownership of fine art, estimated an annual average return of contemporary art at 14% for the period from 1995 to 2020.

However, while these returns may seem attractive, they come with significant caveats.

Lack of data: Art sales happen much less frequently than financial trades.

Randomized perspective: Every piece of art is different. Therefore, it is difficult to compare how one piece sells with respect to another.

Although art indices play a significant role in helping investors better understand the art market, they are poor indicators of the attractiveness of the asset class. Art valuation and pricing are contingent on multiple variables based on the piece of work. Historical pricing data and trends provide ease for analyzing the value and demand of comparable artworks and artists, but it is important to understand the methodology used to construct indices.

The Sotheby’s Mei Moses Indices are widely recognized as the preeminent state-of-the-art market measure. Leveraging over 80,000 repeat auction sales for the same piece over time, Sotheby’s can produce objective art market analyses to complement the world-class expertise of its specialists.

A repeat sale, according to Sotheby’s Mei Moses Indices, compares changes in sale prices of the same artwork at specific points where the painting is sold. The Mei Moses Indices track all live and online auction sales at Sotheby’s, Christie’s, and Phillips for artworks that previously sold at public auction, going back roughly 200 years.

The index creators reasoned that repeat sales are a better way to track price trends for unique objects, such as art because they express price changes of the specific underlying assets rather than the average or median for the market. This helps minimize the effects of infrequent trading, reporting biases, or characteristic differences that can skew the data.

While this methodology provides a sound apples-to-apples comparison of valuation changes, there are multiple tradeoffs:

Selection bias: The Sotheby’s Mei Moses indices represent a tiny percentage of the art market – namely higher value works of art. Hence, these indices need to expand to track the vast majority of the market. Moreover, art price indices are based solely on auction sales, even though private transactions through dealers and galleries make up about half of the art market’s total turnover.

Survivorship bias: Often, only the most successful sales make headlines and are recorded in databases. Many artworks do not appreciate, fail to find buyers, or are sold privately without disclosed prices. This selection effect can give a skewed impression of the average returns in the art market.

Intent bias: There can be a systematic difference between returns realized on purchases in the secondary (or resale) market relative to those in the primary market (when an artwork first comes up for sale, typically through a gallery or the artist’s studio). Prices in the primary market do not necessarily reflect the marginal buyer’s willingness to pay.

Lack of liquidity: Selling an artwork can take considerable time and effort. The average holding period for artworks resold through auction houses is estimated at 25 years. Many are sold below their intrinsic value when the seller needs liquidity.

High transaction costs: Auction houses and galleries often charge 30%-50% fees, and additional costs like insurance, storage, and transportation can eat into profits.

Indices help gauge the art market sentiment and trends. However, they are biased indicators of the investment returns which collectors could get. In contrast to financial asset indices like S&P 500, art indices are not investable and no implementable strategy can replicate index returns. Transaction-based indices typically are based on auction prices only, weigh each transaction equally, and measure geometric average price trends. As a result, they will not accurately capture the investment experience of most art buyers. The noisy transaction prices, positive skewness in returns (combined with long holding periods), and concentration of art collections amplify the problem.

The harsh reality of art investing

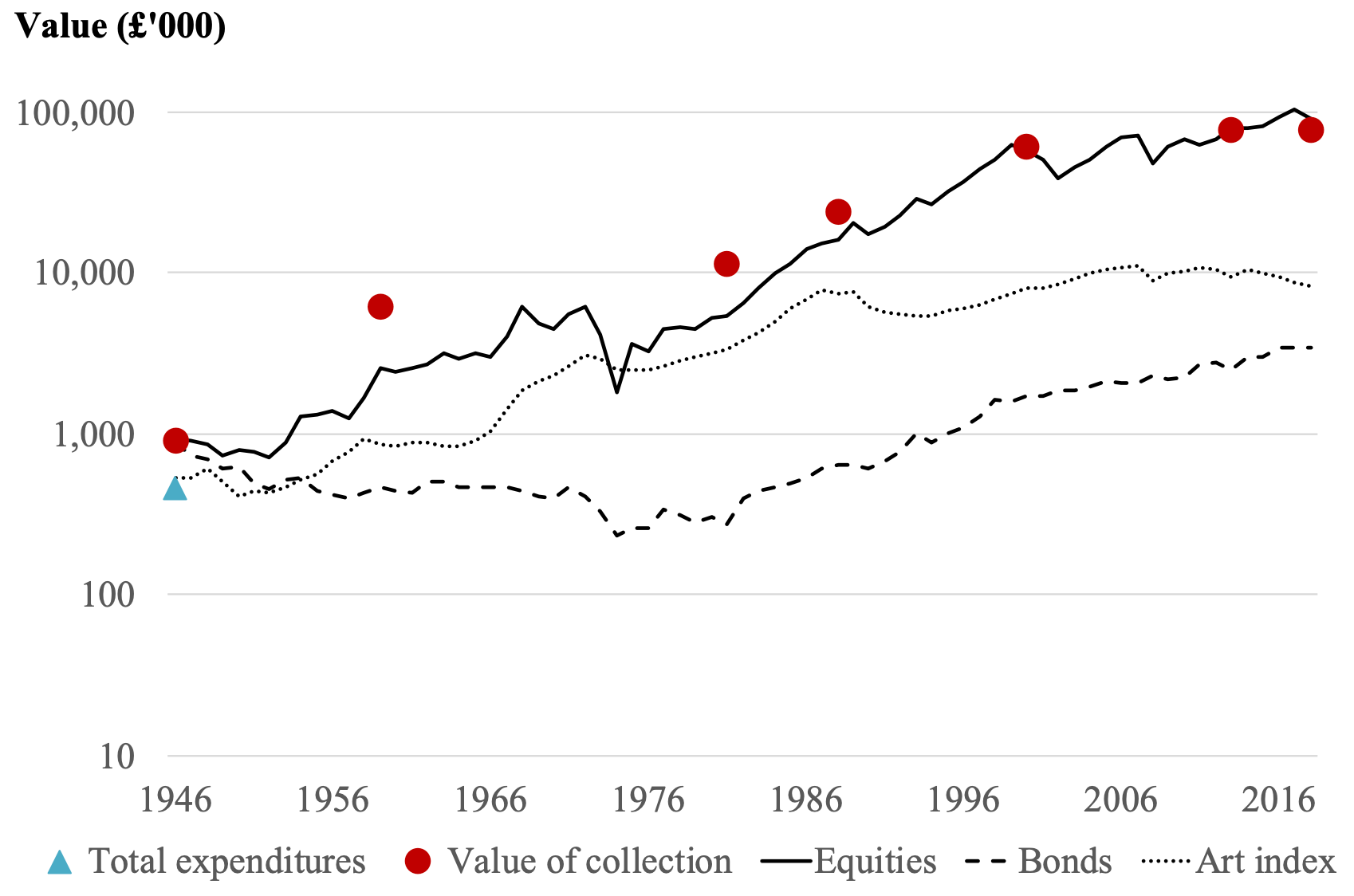

Instead of art indices, one should study portfolios of art over time to understand better the financial returns of the art asset class. A group of researchers from the University of Cambridge examined the long-run buy-and-hold performance of an actual portfolio, namely the collection of John Maynard Keynes.

Keynes is mostly known for his work in macroeconomics government policies. Curious about all financial assets, he accumulated a substantial collection of important artworks which he purchased through various channels between 1917 and 1945. Upon his death, Keynes bequeathed his entire art collection to King’s College in Cambridge. This collection consists of over a hundred pieces by both Modern Masters such as Braque, Cezanne, and Matisse, as well as friends and acquaintances of Keynes like Duncan Grant and Vanessa Bell. The collection has remained intact to the present day, with the pictures being hung at the College and at the Fitzwilliam Museum in Cambridge.

Importantly, Keynes was interested in art as an investment. He carefully and extensively documented his transactions and these records, held at the archives of King’s College. The collection appreciated strongly over time: while Keynes’ total expenditures amounted to less than £13,000, the collection had an estimated market value of more than £76 million in early 2019. This translates into a nominal internal rate of return (IRR) of 10.4% (6.1% in real terms).

The return is impressive. However, it is important to note that it is 0.2% lower than the performance of UK equities during the same period of time. Moreover, the bulk of returns were generated shortly after purchase, suggesting that Keynes was able to buy art at attractive prices. Adjusting for the first 10 years after the artwork purchase, the collection return over the last six decades was only 4.8% per year. Also, just like private equity and venture capital portfolios, Keynes’ portfolio returns were highly concentrated among the few artworks. The ten most expensive purchases represent 80% of his aggregate expenditure on art.

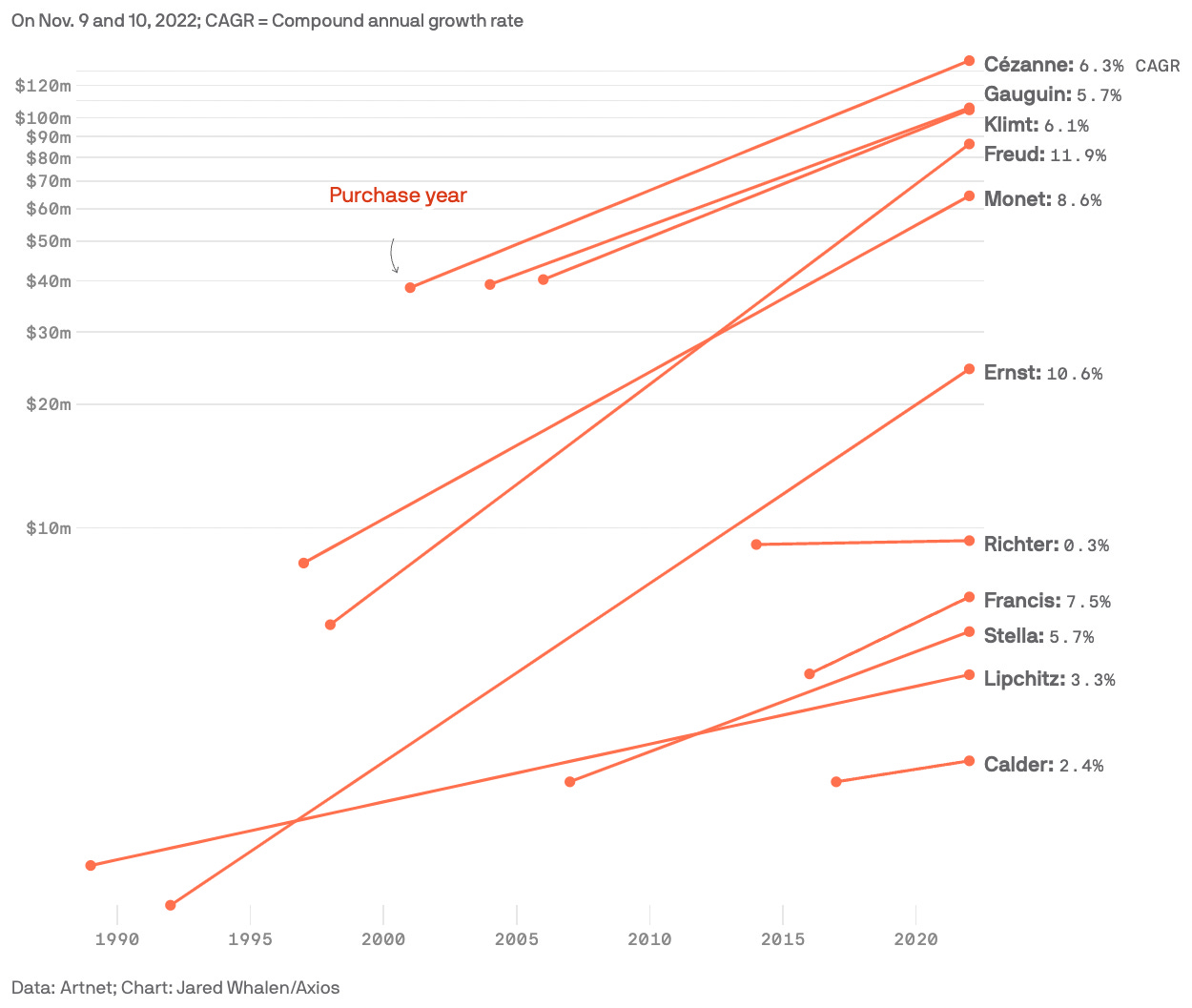

Eight- and nine-figure sales of single artworks certainly make front-page headlines, contributing to the general perception that art investing is profitable. The late Paul Allen’s art collection of 155 artworks fetched $1.6 billion in a record-breaking auction at Christie's in November 2022. Numerous individual pieces sold for more than $100 million each. Georges Seurat’s “Les Poseuses, Ensemble (Petite version)” went for $149 million. The work last appeared on the public market when it sold at Christie’s in 1970, where it realized more than $1 million. Cézanne’s La Montagne Sainte-Victoire, a colourful landscape painted from 1888-1890, sold for $138 million, another record. A Gustav Klimt 1903 painting, Birch Forest, set the high mark for a Klimt work, selling for $105 million. Van Gogh’s Verger avec cyprès sold for $117 million. Paul Gauguin’s 1899 oil on burlap Maternite II fetched $106 million.

These are certainly enormous sales. However, these numbers massively overstate the broader returns to art investment. The average annualized growth rate on the 11 lots with public entry prices was just 6.2%. On average, Allen held them for 18 years before selling them. By contrast, S&P 500 still boasts a compound growth rate of 8.9% over the past 18 years.

Paul Allen is among the top 1% top performing collectors. He was a true visionary, combining a great eye and deep pockets in the 1990s, when first-rate art was particularly cheap. This certainly challenges the notion of art being a great investment.

The double-digit art returns are rare and tend to be prevalent only in the very upper end of the art market. According to the research conducted by the University of Florence, since 2000, contemporary art delivered the highest return, 6%, but also the highest volatility, with a standard deviation of 19%, followed by modern art, with an expected return of 4% and a standard deviation of 14%, and by old master paintings, with an expected return of -1% and a standard deviation of 16%.

Momentum and success stories are a big driver of returns for the rising star contemporary artists. ‘If you had purchased certain established but undervalued female artists in the last five years, such as Rose Wylie RA, who is now with David Zwirner Gallery, you might currently be feeling like art is a great investment,’ says Sarah Barker, partner at the art law firm Withers.

While art can provide substantial returns and diversification benefits, it is not a straightforward investment. It requires a deep understanding of the art market, careful selection, and consideration of various biases and costs. For many, the joy of collecting and appreciating art may be the most reliable 'return on investment' they could ask for. However, for those with a keen eye for talent, an understanding of the art market, and a degree of patience, art can indeed be a lucrative investment.

Select sources:

On the Efficiency of Art Markets Evidence on Return Rates from Old Masters Paintings to Contemporary Art, University of Florence

Art as an Asset: Evidence from Keynes the Collector, research paper by David Chambersa, Elroy Dimsonb, and Christophe Spaenjersc

Buying Beauty: On Prices and Returns in the Art Market, research by Luc Renneboog and Christophe Spaenjers

The Artprice100 index of Blue-chip artists up 3% over 2022, Artprice

Investing in the Art Market: A $1.7 Trillion Asset Class, CAIA

Paul Allen's art didn't outperform the stock market, Axios

Art Indices & Why They Matter, Masterworks

The Art Market 2023, Art Basel & UBS

Investing in culture also changes the world around you.